Meet Your New Marketing Team: the Regulators

For little-known companies struggling to introduce a new product, regulatory pressure can offer an unexpected benefit: a halo of legitimacy that marketing money can’t buy.

While many might argue compellingly that regulation protects the public, regulated industries have often complained that it stifles innovation. In industries ranging from pharmaceuticals to banking to energy, regulation affects how new products are developed and marketed, how plants are built, how businesses are acquired and how daily operations are conducted.

But for little-known companies struggling to introduce a new product, regulatory pressure can offer an unexpected benefit: a halo of legitimacy that marketing money can’t buy.

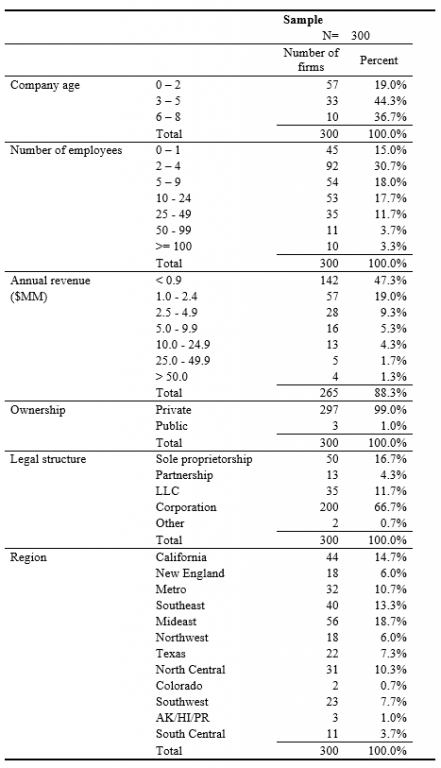

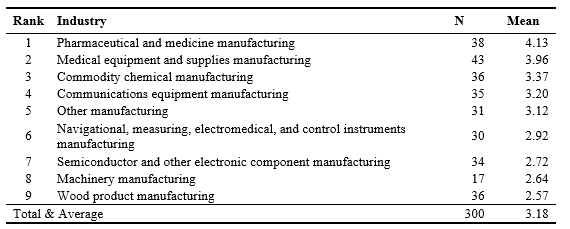

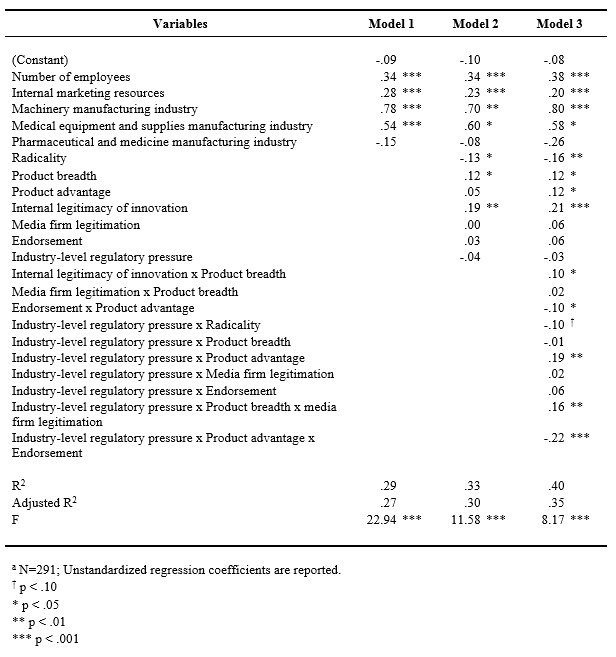

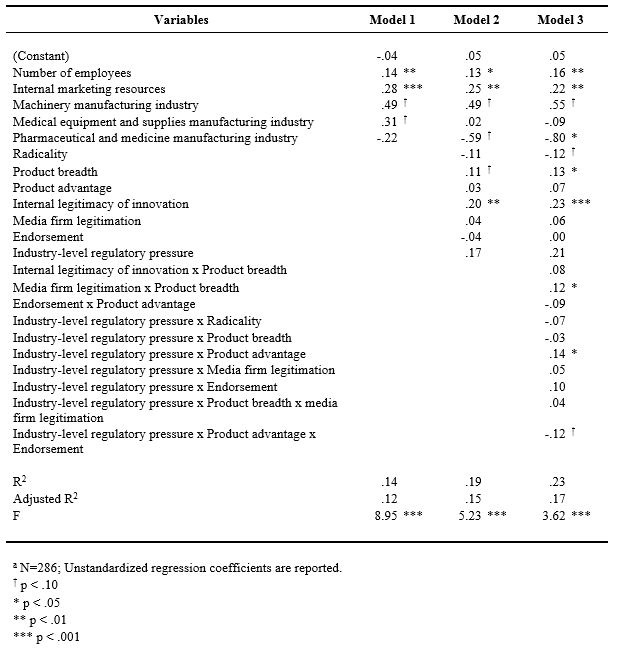

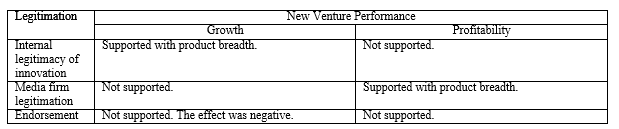

Those were the findings of a study of 286 entrepreneur-run firms by a trio of professors: David Deeds of the University of St. Thomas; Bill Schulze of the University of Utah and Yasuhiro Yamakawa of Babson College. They studied firms from eight industries, ranging from the highly regulated (pharmaceuticals and medicines) to the largely unregulated (wood products manufacturing.) Most of them were relatively unknown and had fewer than 10 employees.

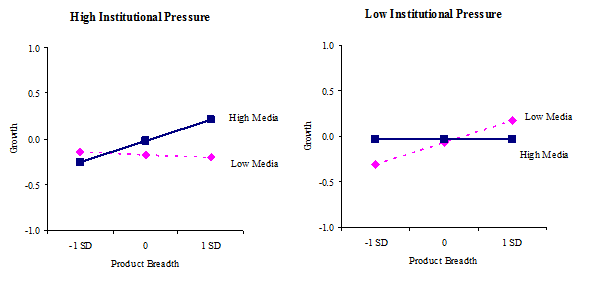

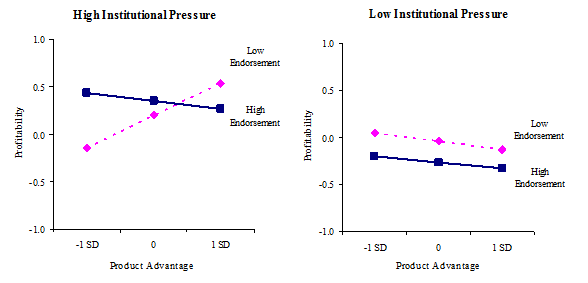

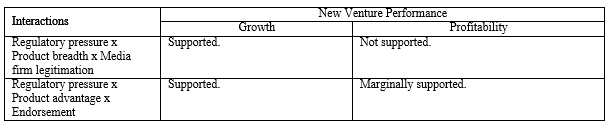

“What we found was that in a highly regulated industry, a new product with substantial advantages didn’t need media coverage and endorsements once it was approved by regulators,” said Deeds. “Just getting the product approved was enough. But in industries that were unregulated, the companies needed outside endorsements and positive media coverage a lot more.”

Most entrepreneurs face formidable obstacles to bringing a product to market, including a big one that academics call “the liability of newness.” It is difficult for an upstart product from an unknown company to achieve “legitimacy,” or recognition from potential investors, influencers and customers that it is valid and useful. Moreover, as the report points out, the companies that make more established competing products can deploy staff and other resources to discredit the upstart.

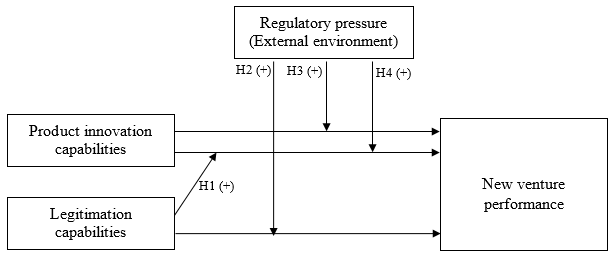

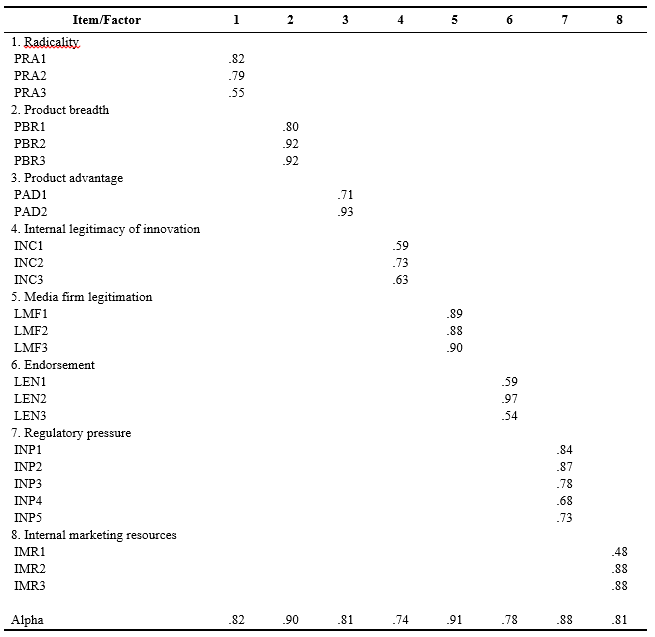

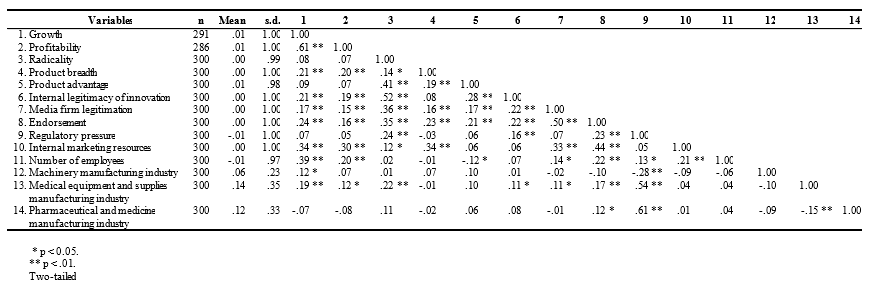

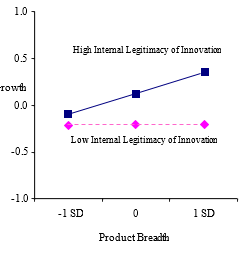

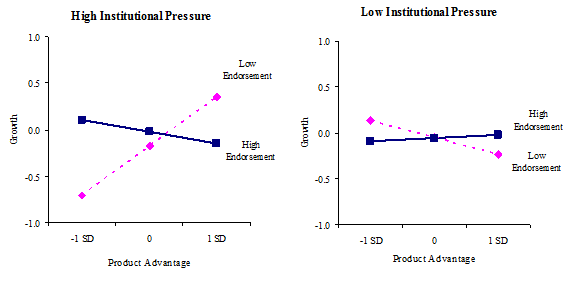

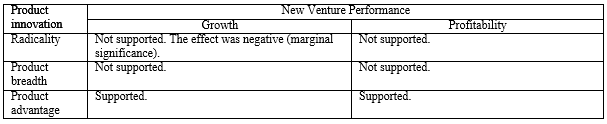

The study looked at the interplay between product innovation, regulatory pressures, and the degree of external networking (including courting the media and getting endorsements.) Respondents answered questions about how radical their products were; the degree of positive press coverage; the connections they have with prominent individuals and organizations; the degree of regulation they face; and whether they spend more on marketing than their competitors.

Researchers found that for the companies in regulated industries, the regulation process vets the new product enough to make it legitimate in the eyes of others. Any product that clears the hurdles is deemed trustworthy, because others have tested it and verified it’s the real thing. For example, a new drug that’s received Food and Drug Administration Approval has a better chance that doctors will accept it, even if the manufacturer is relatively unknown.

On the other hand, the respondents in unregulated industries said they needed more help from influencers to give their products legitimacy.

“In a less regulated industry it’s considered less of an accomplishment to introduce a new product to the market,” Deeds points out, adding that this means that the product will be suspect until outsiders – the press and other influencers – endorse it.

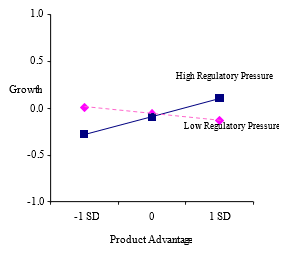

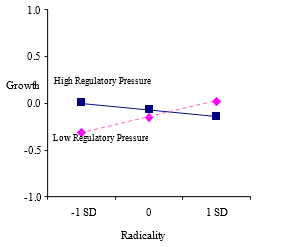

And even in regulated industries, getting approved is not enough if the product is not novel enough or substantially better than others already on the market, the study found. For example, if a new drug is too similar to other ones, the manufacturer still needs to spend some money to attract endorsements and demonstrate why it’s different.

“These findings are important because new ventures often have limited resources when they are trying to get new products to market,” Deeds says. “Entrepreneurs and those who invest in them should understand which investments in capabilities can bring them the best return on their time, energy and money.”

The Takeaway

- Companies operating in a strong regulatory environment, like pharmaceuticals and medical devices, should spend their money building an outstanding product and getting it through the regulators. But if you’re making wood products or another unregulated product, save your money for campaigns that attract outside endorsement.

- Regulated products that are too radical may still need some public relations help, even after they win approval. You may need some influencers to demonstrate why your product is useful and to give it legitimacy.

- Likewise, a “me too” product – one that’s too similar to something else in your product line or to another company’s product -- may skate past regulators but will still need a public relations and media push to attract notice. The product has to be substantially better or substantially different for the approval to give it legitimacy.

- If you’re an investor looking at small entrepreneurial firms offering promising new products, invest during the development phase if it’s a regulated industry and in the marketing phase if it’s unregulated.

Additional search terms: getting my product approved, getting regulators to approve my product, government red tape, fighting with regulators, FDA, drug approvals

.

.

View Profile

View Profile

View Profile