Technical Specialized Knowledge and Founder Leadership at Initial Public Offering

In 2003 Noam Wasserman introduced the term “Paradox of Success” to describe how software company founders were more likely to be replaced as their startups attracted more capital or went public. Using a sample from multiple industries, this new study has looked more closely at which types of founders were more likely to survive these success milestones.

What is the secret to their staying power? They have deep knowledge that is important to their company’s commercial success and that is hard to share with others.

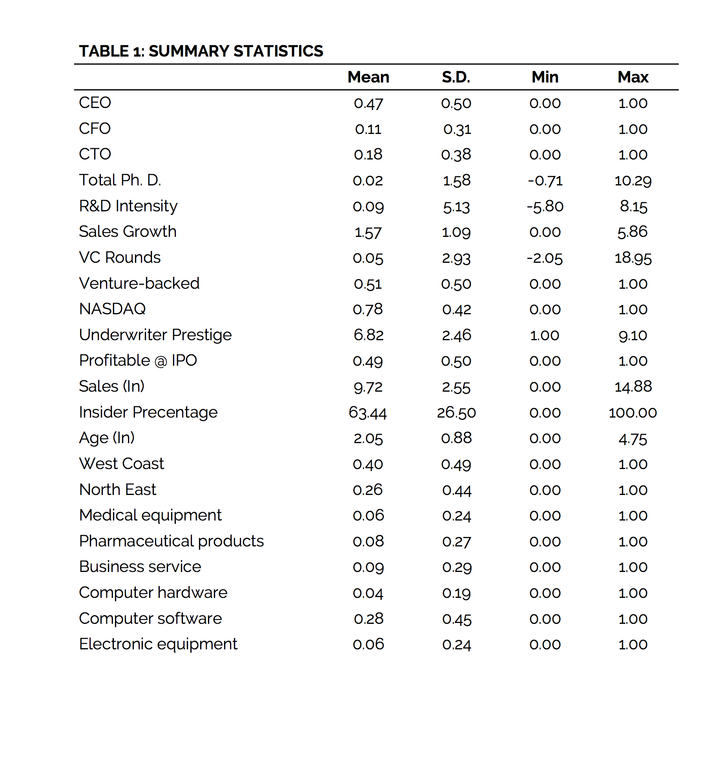

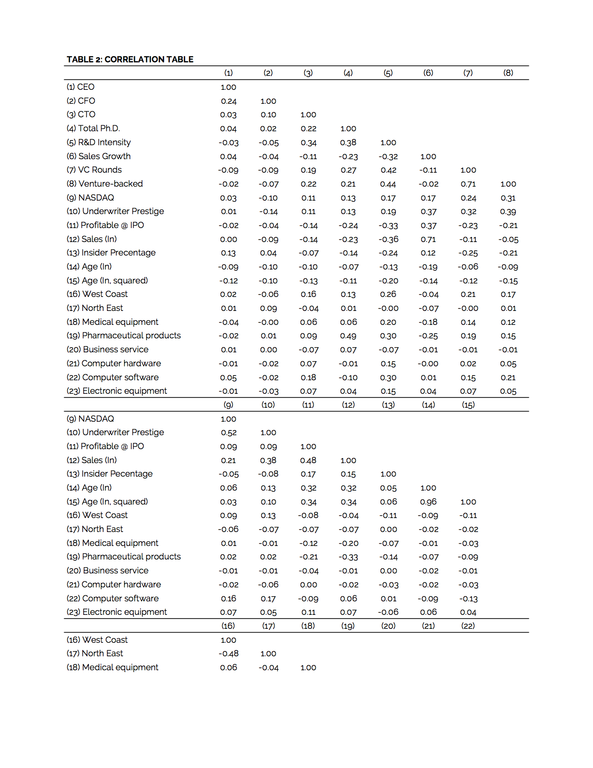

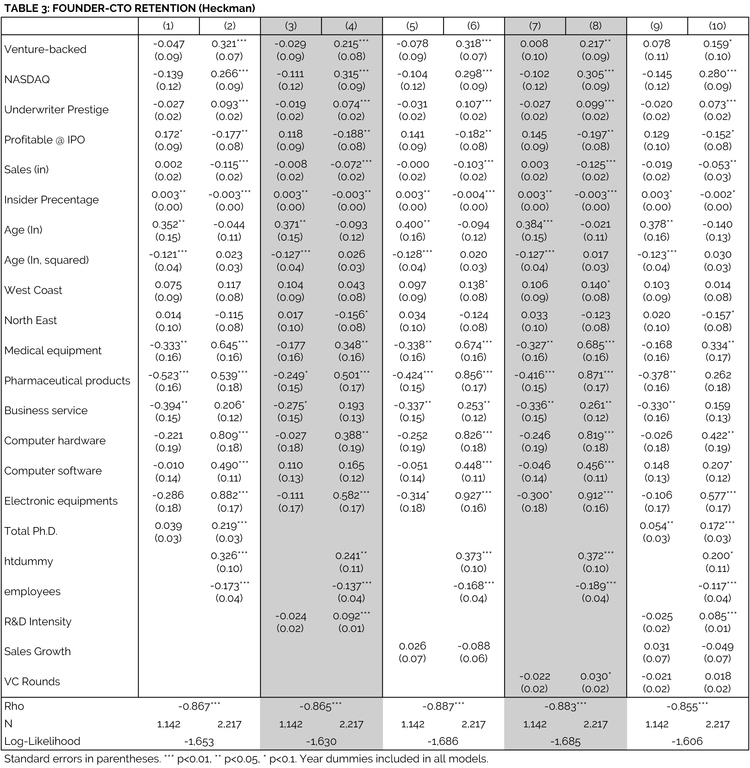

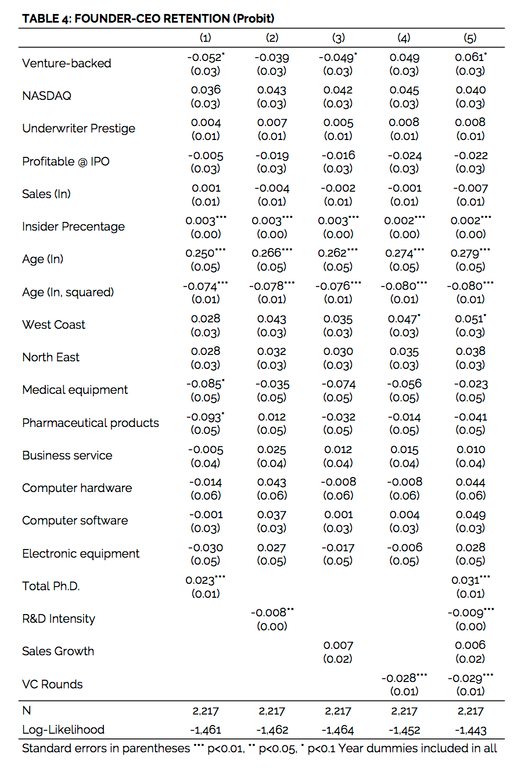

Entitled “Technical Specialized Knowledge and Founder Leadership at Initial Public Offering,” our comprehensive historical study looked at more than 2,000 firms representing most industries that completed an IPO from 1992 through 2002. We analyzed whether the companies’ founding chief executive officers (CEOs), chief financial officers (CFOs) and chief technical officers (CTOs) remained past the IPO. We found that in firms where science is a key part of commercial success, the founding CEOs, CFOs and CTOs with the deepest knowledge tended to have greater job security.

We looked at how much these firms relied on Technical Specialized Knowledge (TSK) for their commercial success. TSK is gained after years of education and experience working on difficult problems and hence is not easily transmitted to others lacking similar experiences and education. Even fellow top executives might have a hard time comprehending what the founders deeply understand.

Science is highly specialized -- some microbiologists can’t understand what other microbiologists are doing if they have not been working on the same research questions. For some science and technology companies, the founders’ TSK is the key to firms’ current success and their future growth. They can’t be replaced easily.

Other types of firms don’t seem to use TSK at all—or at least at IPO. The study notes that Starbucks Corp., when it went public in 1992, conducted no R&D and had no PhDs among its founders at the time -- but another firm studied, Watson Pharmaceuticals, had five PhDs among its top management team.

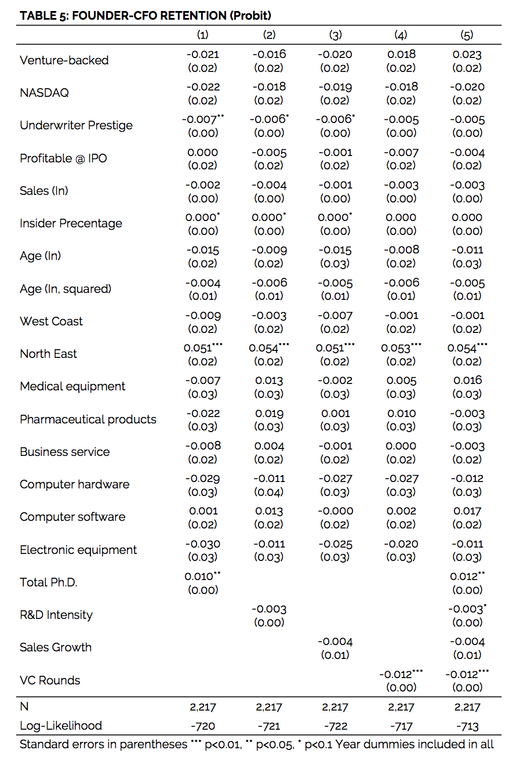

Our study treats R&D as the search for new knowledge, an activity that firms that don’t use TSK also conduct. Our research suggests that the effect of R&D on founder turnover is different from the presence of TSK. R&D spending did make some founders more vulnerable. CTOs were more likely to survive in companies that spent heavily on R&D, but CEOs and CFOs were more likely to leave. R&D tends to create a more complex firm that requires more generic management skills, outside of the CTO role. The investors and board directors may put pressure on the firm to have CEOs and CFOs with these broad skills at the helm.

The study did not find broad support for Wasserman’s paradox of success. For example, an important metric of success for young innovative companies is revenue. Wasserman’s logic suggests that founders are more likely to be removed from executive jobs when revenue is growing rapidly. Our research however, did not find such an effect. Our study did find some support for Wasserman’s argument that founders are less likely to remain in executive positions if they raise additional rounds of capital. While raising capital is often viewed as a successful outcome by managers, it can also be viewed as a negative outcome if capital was needed to be raised as a result of poor management.

The Takeaway

- If you’re a founding entrepreneur, someday you may not have a choice as to whether you stay with the company you founded. Having technical specialized knowledge (TSK) may help you hang on past the new capital and IPO.

- Sales growth is no guarantee that you as a founder will remain in an executive position but it doesn’t make you more vulnerable either.

- If your firm is starting to do more R&D, you could lose your job if your specialized knowledge is not critical to the new areas of knowledge being explored.

Additional Search Terms: Founders getting kicked out of their own companies, founders losing control of company at IPO, investors taking over, keeping control of my company

View Profile

View Profile

View Profile