Crowdfunding, Entrepreneurship, and Start-Up Finance

Note: This is the first of two articles that explore crowdfunding's emergence as an important source of capital for entrepreneurs and others; its history and an overview of how the major crowdfunding platforms work.

For entrepreneurs, attracting capital to finance their entrepreneurial dream is the most significant challenge and struggle, at least initially. A survey by the Kauffman Foundation stated that in 2014, 67% of the funding that drove the 5,000 fastest-growing firms listed by Inc. Magazine came from personal savings (Wiens and Bell-Masterson, 2015). According to the authors, other sources of entrepreneurial funding included family (20.9%), friends (7.5%), venture capitalists (6.5%), government grants (3.8%) and angel investors (7.7%). While these traditional sources of capital funding remain popular with entrepreneurs, the phenomenon of crowdfunding has introduced an alternative source of startup finance. Terry, Schwartz, and Sun (2015) reported that start-up financing through crowdfunding grew from $1.5 billion in 2011 to $10.0 billion in 2014. By 2017 Kaartemo (2017) estimated that the global crowdfunding industry was worth $34 billion and was projected to grow to $300 billion by 2025.

Both equity and non-equity crowdfunding have proven to be productive methods of capital formation for start-ups The equity crowdfunding provisions of The Jumpstart Our Business Startups Act (the “JOBS” Act) offer perhaps the most promising development to the facilitation of capital formation for entrepreneurs since the Great Depression. The JOBS Act became law in April 2012 and established a regulatory foundation enabling startups and small businesses to access new capital using crowdfunding. (“Updated: Crowdfunding and the JOBS Act: What Investors Should Know”, n.d.). Title III of the JOBS Act, known by the acronym THE “CROWDFUND” Act (Capital Raising Online While Deterring Fraud and Unethical Non-Disclosure Act) creates an exception that allows U.S. securities laws to be amended to allow equity crowdfunding campaigns to be easily employed to raise capital. These crowdfunding-related provisions articulate an evolving process of gathering funds outside traditional means via the Internet for projects, including artistic endeavors and innovative product ideas. Title III of the JOBS Act devised an exception in the securities laws that enabled this type of funding to be used to tender and sell securities. Through this Act, Congress intended to assuage the funding gap, and lower regulatory barriers for startups and small businesses by letting them raise capital from a larger pool of investors (SEC Issues Proposal on Crowdfunding, 2013). While crowdfunding has become a fast-growing avenue that provides capital funding for entrepreneurial start-up ventures, many need a deeper understanding about how it works and what it can achieve.

History of Crowdfunding

Crowdfunding can be defined as “the practice of funding a project or venture by raising money from a large number of people who each contribute a relatively small amount, typically via the Internet: musicians, filmmakers, and artists have successfully raised funds and fostered awareness through crowdfunding” (Crowdfunding, n.d.). Bradley and Luong (2014) wrote that the concept of crowdfunding can be traced to 18th-century Ireland when loans were given to low-income families, primarily in rural areas, to finance home ownership. Called the "Irish Loan Fund," these investments were popular throughout the 1800s, when 20% of all Irish households were financed using this model. The "Irish Loan Fund" notion of low-income financing eventually made its way to India, where Nobel Prize-winning economist Mohammad Yunus' concept of "microfinancing" served as the genesis of modern-day crowdfunding. By providing $27 in seed money to 42 poor women to begin making and selling bamboo furniture, Yunus created opportunities for self-employment and curtailed consistent exploitation of the poor (Clark, 2011). After recouping his investment and demonstrating the viability of mini-loans to the poor, Yunus secured capital from central banks and foundations to extend the project to others. Yunus's microfinance idea made the leap from a small, localized program to what is known today as the Grameen Bank, with a clientele of over 8 million borrowers, 97% of them female-operated businesses (Bradley & Luong, 2014).

Today, crowdfunding has evolved to meet the fundraising needs of non-profits, entrepreneurs and independent creative artists of all types (film, game developers, music, theater, et al.), generally employing a donation or rewards incentive model. In 1997, the British rock band Marillion managed to raise $60,000 primarily through online donations to finance a hoped-for farewell tour. Marillion’s success in raising the required capital led to the formation of ArtistShare in 2000, which according to Bradley and Luong (2015) was the original crowdfunding platform to enable artists’ fans to donate to various projects. The ensuing decade witnessed the spawning of additional crowdfunding entities including Kiva, started in 2005, which provided small loans to entrepreneurs in poor areas around the world; Prosper, founded in 2006, the first peer-to-peer lending marketplace in the U.S.; Indiegogo, begun in 2008, enabling people to donate more easily by eliminating the middleman; Peerbackers, started in 2008 with the intent to raise money online to meet a funding goal in exchange for rewards or perks; and Kickstarter, in 2009, a funding podium for innovative projects by fans, friends and the public in return for rewards (Clark, 2011).

In 2012 President Obama signed the JOBS Act into law (The History of Crowdfunding, n.d.). This groundbreaking piece of legislation changed the landscape for crowdfunding platforms. Before April 5, 2012, when the JOBS Act became law, existing crowdfunding entities were allowed only to function on a reward or donation basis. This meant that crowdfunding platforms could offer only a discount, a product, or an enticement in return for monetary funding. The JOBS Act opened the door for the general public to receive equity in an enterprise in exchange for funding (Prive, 2012). Shortly following the law's enactment, FUNDABLE, an equity crowdfunding platform, was launched to assist entrepreneurs in financing and building their businesses through equity crowdfunding (The History of Crowdfunding, n.d.)

While much of the scholarly research to date has been focused on the United States, crowdfunding is a worldwide phenomenon, impacted by the different experiences and legal frameworks of every jurisdiction (Giudici, Nava, Lamastra, & Verecondo, 2012). Dushnitsky, Guerini, Piva and Rossi-Lamastra (2016) argued that in Europe, crowdfunding has the potential for worldwide access and that crowdfunding is not the sole domain of startups. Existing organizations can tap this resource as the industry continues to expand and grow in sophistication.

Crowdfunding and Entrepreneurship

Entrepreneurship is defined as “the activity of setting up a business or businesses, taking on financial risks in the hope of a profit” (Entrepreneurship, n.d.) Kaartemo (2017) stated that recently, crowdfunding has emerged as a significant force in financing both entrepreneurial and nonprofit enterprises. Vealey and Gerding (2016) supported this notion, writing that crowdfunding has altered the landscape of what it means to be an entrepreneur. While pursuing the entrepreneurial dream will likely continue to be a lonely task, crowdfunding has made it possible for entrepreneurs to appeal to the public for startup funding rather than chase venture capitalists, angel investors, banks, friends and family, or maxing out credit cards. The consequence of this phenomenon, according to Vealey and Gerding (2016), is that the breadth of entrepreneurial activities has expanded from the traditional for-profit opportunities and now includes cultural, social and civic issues that affect the community.

Li, Chen, Kotha, and Fisher (2017) note that crowdfunding offers entrepreneurs the ability to seek initial funding for an enterprise that, in its infancy, may not catch the eye of traditional financing venues. Bankers, venture capitalists, and angel investors typically possess the financial savvy to adequately assess an entrepreneurial idea, while crowdfunding endorsers are often investment neophytes who are driven by a cause or passionate about an idea, product or service. New ventures require professional legal guidance (Trautman, Luppino & Simmons, 2016). Both non-profit and for-profit entities must provide for a legal governance structure before funding (Trautman, 2013; Trautman & Ford, 2018). The rapid rate of technological change brings novel challenges to early-stage enterprises as they seek funding (Trautman, 2016a; Trautman, 2016d; Trautman & Harrell, 2017; Trautman, 2018a and b; Trautman & Ormerod, 2018; Trautman & Molesky, 2019; Trautman & Ormerod, 2019). Social media has become a driving force behind the exploding growth of crowdfunding, requiring the attention of management and the board (Trautman & Michaely, 2014; Trautman 2016 b and c; Trautman, 2017). However, social media has not been a factor for the more traditional forms of financial backers. The breathtaking rise of crowdfunding and the continuing evolution of entrepreneurial funding create the need to examine further where crowdfunding fits in entrepreneurial funding.

Crowdfunding Finance

New entrepreneurial startups are an integral part of the economy. According to a study by the Kauffman Foundation, entrepreneurial ventures account for as much as 50% of all new job creation (Kauffman Foundation, 2016). Additionally, successful entrepreneurial startups expand not only in size but create new jobs in varied geographic locations. The Center for Rural Affairs wrote that entrepreneurship is the most desirable strategy for rural economic development. In Nebraska, for example, over 70% of net new job creation is the result of people creating their own non-farm related jobs (Center for Rural Affairs, n.d.). Mazerov (2016) reported that while about half of all new startups fail within five years, many turn into fast-growing enterprises with job growth of 20% to 25% or more. Entrepreneurial startups created approximately 3 million jobs per year between 1980 and 2010. Half those jobs may no longer exist, but the other half remained. The firms that survived grew substantially during their first five years of existence, averaging 60% growth, adding another 900,000 jobs to the economy (Mazerov, 2016). The importance of entrepreneurial startups in our economy cannot be overstated.

Entrepreneurs historically have followed a traditional path chasing initial funding for their ventures. These sources typically included self-financing, grants, angel investors and venture capitalists (Cornell, 2014). Exhibit 1 displays the traditional funding sources for early-stage ventures.

Exhibit 1

Traditional Funding Sources for Early Stage Ventures

|

|

Self-Funding (Friends & Family) |

Grants |

Angel Investors |

Super Angels |

Venture Capital |

|

Overview |

Usually adds no value to the venture other than cash |

From business plan competitions, university innovation/entrepreneurship programs, economic development grants

|

Accredited investors investing as individuals or in groups |

Accredited individual investors with significant investing experience who take active roles |

Institutional funding (managed by professional investors) |

|

Typical Range |

Less than $20,000 |

$5,000 - $100,000 |

$150,000 – $15 million |

$250,000 – $15 million |

$5 million - $50 million |

|

Annual $$ Invested |

$50 billion |

$3 billion |

$20 billion |

$0.2 billion |

$20 billion |

|

Stage |

Idea, seed, pre-seed |

Pre-seed, start-up |

Most for startups and growth stages

|

Startup and growth stages |

Startup, most for growth and later stages

|

|

Obstacles & Issues |

Younger entrepreneurs lack sufficient self-funding or resources from friends |

Require significant time and preparation |

Requires evidence of market validation and traction |

Same |

Fund companies, not ideas. Requires significant commitment, an issue for student entrepreneurs |

Traditional funding sources (Cornell, 2014/Payne, 2011)

Mollick (2014) contends that crowdfunding now supports not only relatively small artistic and creative type efforts, but also a more extensive range of entrepreneurial projects. The concept in both cases is the same: Raise capital from a large number of contributors who put forth small contributions via the internet (Cornell, 2014). Crowdfunding has changed the sources traditionally utilized for funding new entrepreneurial ventures. Exhibit 2 displays the various facets of crowdfunding efforts.

Exhibit Two

The Many Facets of Crowdfunding

|

|

Donation Crowdfunding |

Rewards-Based Crowdfunding |

“Pre-Order” Crowdfunding |

P2P Lending |

Equity Crowdfunding |

|

Overview |

Generally for causes and charitable fundraising |

Most popular: people pledge contributions in return for “token” rewards (emotional or affinity based). |

Rapidly rising in popularity. Early funders get advance or early versions of the product. |

Peer to Peer lending. “The crowd” loans money |

The general public invests small amounts in return for stock.

|

|

Typical Range |

Under $10,000 (often under $2,000). |

Varies widely. Average $7-10k per project. But many attract $50k, $100k |

Varies widely; many projects attracting over $100k, to $1-$5 million. |

Usually for “micro-loans” for small business >$2,500. |

New SEC regulations. Practical for over $500k to $5m or greater |

|

Typical Candidate

Projects |

Charitable causes, events. |

Creative projects, events. |

New product innovations. |

Small business. |

Established startups (post-seed) |

|

Advantages |

Allows entrepreneurs to efficiently solicit funding from friends and family (who primarily want to help the entrepreneur, personally) |

Solicits funding from advocates passionate about the idea, as well as feedback and advice. |

Pre-order (advance sales) provide valuable market validation as well as product funding |

Funding for small business that otherwise would not qualify for bank loans |

Circumvents the venture capital industry and allows for raising significant funding by going directly to the public. |

|

Dis-Advantages |

Practical for small amounts only |

Practical for nominal fundraising, but does not prove customer demand. |

Pre-order commitments can be very risky (selling a product that does not yet exist). |

P2P lending requires repayment, and usually personal guarantees. |

Significant overhead costs in preparing, regulations still in flux. |

The Many Facets of Crowdfunding (Cornell 2014)

Husain and Root (2015) argue that a significant number of entrepreneurial startups cannot access the necessary financing they require to grow and that crowdfunding provides entrepreneurs a path to bridge the gap between early-stage financial needs and the capital required for long-term growth. Husain and Root (2015) contend that the 2008/2009 global recession created a scenario in which banks were reluctant to lend to early-stage businesses and often forced fledgling entrepreneurs to spend inordinate amounts of time in the application process rather than operating their business. The authors argue that an additional benefit of crowdfunding is that it provides a window for more traditional types of entrepreneurial funding -- including venture capitalists, angel investors, and even banks -- to discover startups they would have likely not found otherwise. With the value of crowdfunding campaigns firmly established in the literature, we next examine two of the larger crowdfunding platforms to gain a sense of how they operate and fit into the overall scheme of entrepreneurial financing.

Kickstarter

Kickstarter has emerged as the largest crowdfunding platform that entrepreneurs of an artistic or creative nature can employ to seek financing for their projects (Moreau, 2018). Kickstarter utilizes an all-or-nothing funding model. If the entrepreneur’s project does not reach 100% of its goal, the funds are not collected, and no exchange of money takes place (Funding, n.d.). According to Zouhali-Worrall (n.d.), successful projects pay 5% of funds raised to Kickstarter, and they also pay 3% to Amazon Payments, the organization that processes contributions. Mollick (2016) reports that individuals are responsible for creating two-thirds of all Kickstarter projects, with about a third by teams. Average team size is 3.1 members, with friendship the most reported relationship, followed by spouses. Most project creators are reported to be between 25-34 years of age, with an average age of 38; 41% are female; and 83% non-Hispanic whites.They are generally highly educated: 82% are college graduates, of which 34% hold advanced degrees (Mollick, 2016).

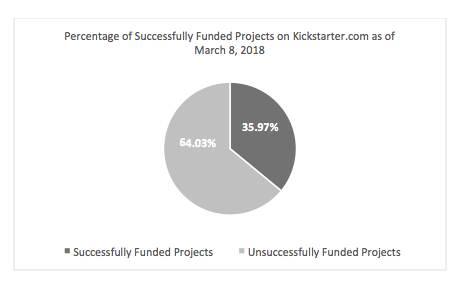

Kickstarter reports that as of March 8, 2018, 140,135 projects have achieved successful funding, receiving pledges of $3.5 billion. 17,363 projects raised less than $1,000; 77,964 raised $1,000 to $9,999; 20,204 raised $10,000 to $19,999; 19,766 raised $20,000 to $99,999; 4,560 raised $100K to $999,999; and 278 raised $1 million (Stats, 2018). Exhibit three displays the percentage of projects successfully funded through Kickstarter as of March 8, 2018.

Exhibit Three

Percentage of Successfully Funded Projects on Kickstarter.com as of March 8, 2018.

Stats, 2018

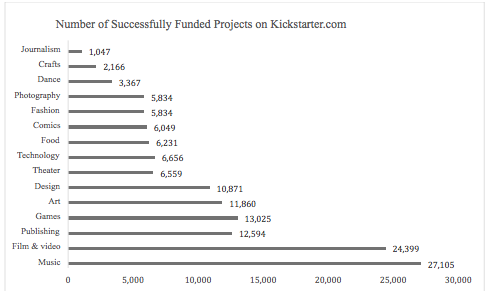

With only 14.1% of non-artistic type projects funded by Kickstarter.com (journalism, technology, and publishing), Kickstarter.com has become one of the go-to crowdfunding platforms for creative and artistic entrepreneurial ventures. As of March 8, 2018, exhibit four displays the number of Kickstarter projects successfully funded by category.

Exhibit Four

Number of Successfully Funded Projects on Kickstarter.com

As of March 8, 2018, By Project Category

Stats, 2018

Indiegogo

Danae Ringelmann, Eric Schell, and Slava Rubin founded Indiegogo after struggling to find a solution to the problem of optimizing the crowdfunding process and making capital-raising campaigns more widely available. Indiegogo was launched in 2008 and has assisted with over 800,000 creative ideas with more than 9 million supporters (About Us, n.d). Indiegogo offers entrepreneurs two types of crowdfunding campaigns: fixed and flexible. With fixed funding campaigns, the entrepreneur receives the money raised only if the funding goal is fully achieved. If the goal is not achieved, Indiegogo refunds all monies within five to seven business days. In contrast, flexible funding campaigns allow the entrepreneur to keep the money raised regardless of whether the funding goal of the campaign is achieved (Choose Your Funding Type, n.d.). For fixed campaigns, Indiegogo charges 4% of the total funds raised along with a 3% to 5% credit card processing fee. For flexible campaigns, Indiegogo charges 4% if the total funding goal is achieved and, should the funding goal not be reached, 9% plus a 3% to 5% credit card processing fee (Choose Your Funding Type, n.d.). To expand its operations, Indiegogo created "Generosity," a fundraising site designed to raise money for personal or social causes that charge no platform fee but levies a 3% payment processing charge and 30 cents per-donation fee (Cowley, 2015).

Indiegogo does not disclose a full range of statistics including product category, or the number of successful campaigns. In 2017, Indiegogo launched a total of 98,000 campaigns with 1.9 million total backers providing 24 million contributions (Looking Back, 2017).

Differences Between Kickstarter and Indiegogo

These two giants of the crowdfunding industry have four primary differences:

1) Kickstarter accepts backers from around the globe but initiating projects is available to individuals only from the U.S., UK, Canada, Australia, New Zealand, Netherlands, Denmark, Ireland, Norway, Sweden, Germany, France, Spain, Italy, Austria, Belgium, Switzerland, Luxembourg, Hong Kong, Singapore, Mexico and Japan who meet the site's terms of use (Creator Questions, n.d.). In contrast, Indiegogo considers itself an international crowdfunding site where an entrepreneur from anywhere in the world can raise money for a wide variety of projects (Moreau, 2018).

2) Indiegogo offers more project categories than does Kickstarter. Possibilities include: animals, art, comics, community, dance, design, education, environment, film, food, gaming, health, music, photography, politics, religion, small business, sports, technology, theater, transmedia, video, web and writing. Of the top 20 most-funded projects, the top 10 are either technology or design (Shopify, n.d.). Kickstarter is the largest crowdfunding platform for projects of a creative nature (Moreau, 2018).

3) Kickstarter follows the fixed funding model that requires payment only if the project fundraising goal is achieved. Indiegogo offers both fixed and flexible funded campaigns (Shopify, n.d.).

4) Kickstarter requires the approval of an application that assures the campaign is about a project that falls under their categories. Indiegogo has no such application process. Anyone can initiate a campaign without approval. Create a campaign and get started (Moreau, 2018).

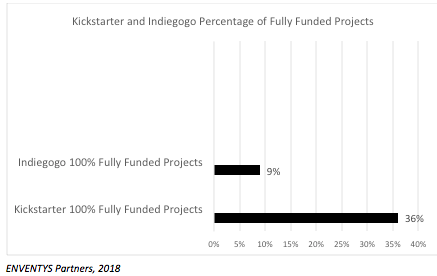

Not All Crowdfunding Campaigns Are Successful

Most crowdfunding campaigns are not totally successful. Clifford (2016) stated that the majority of crowdfunding campaigns do not meet their monetary goals. Kickstarter reports a 36% success rate of reaching 100% of the funding goal (Stats, 2018). According to Clifford (2016), in 2015, Indiegogo achieved a 13% success rate with projects achieving 100% of their funding goal. Exhibit five displays the fully funded (100%) success rate of these two crowdfunding giants.

Exhibit Five

Kickstarter and Indiegogo Fully Funded (100%) Projects

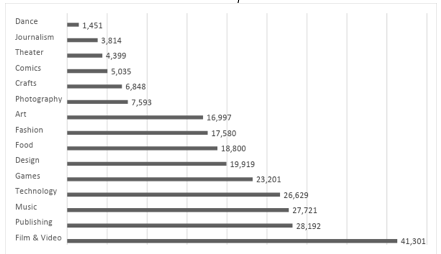

As of March 8, 2018, Kickstarter reports that 249,532 projects failed to achieve their funding goals, and 21.7% of Kickstarter projects finished their campaign without receiving even a single pledge (Stats, 2018). Several factors are attributable to the discrepancy between crowdfunding platform success rates. The funding model (fixed or flexible), restrictions regarding the type of project, length of the campaign, proper exposure by the platform of choice, the momentum behind the campaign, and the effective utilization of social media to promote the campaign (How likely is your crowdfunding campaign to succeed?, n.d.). Exhibit six displays the number of unsuccessfully funded Kickstarter projects by project category.

Exhibit Six

Number of Unsuccessful Projects on Kickstarter.com

As of March 8, 2018, By Project Category

Stats, 2018

Conclusion

Part one of our two-part article has presented a few thoughts about the history and evolution of crowdfunding and how artists and entrepreneurs have successfully used crowdfunding as one of several methods of attracting capital. In our next installment (part two), we look at how regulations are evolving in response to these new funding mechanisms and the rapid technological change that is making them possible.

References

Arnold, M.T. (1985). The definition of a security under the Federal Securities Law Revisited. Cleveland State Law Review. Retrieved from https://engagedscholarship.csuohio.edu/cgi/viewcontent.cgi?referer=https://www.google.com/&httpsredir=1&article=1967&context=clevstlrev

Blue Sky Laws. (n.d.). In The Free Dictionary. Retrieved from https://legal-dictionary.thefreedictionary.com/blue+sky+laws

Bradley, D.B., & Luong, C. (2014). Crowdfunding: A new opportunity for small business and entrepreneurship. Entrepreneurial Executive. (19), pp. 95-104. Retrieved from https://scholarworks.waldenu.edu/cgi/viewcontent.cgi?article=4860&context=dissertations

Brummer, C. (2015). Disruptive technology and securities regulation. Fordham Law Achieve of Scholarship and History. Retrieved from https://ir.lawnet.fordham.edu/cgi/viewcontent.cgi?article=5158&context=flr

Center for Rural Affairs (n.d.). Strategy#2: Small Entrepreneurship. Lyons, NE.

Choose Your Funding Type. (n.d.). Retrieved from https://support.indiegogo.com/hc/en-us/articles/205138007-Choose-Your-Funding-Type-Can-I-Keep-My-Money-About Us,

Choose Your Funding Type. (n.d.). Retrieved from https://support.indiegogo.com/hc/en-us/articles/205138007-Choose-Your-Funding-Type-Can-I-Keep-My-Money-

Clark, B. (2011, Sept. 15). The history and evolution of crowdfunding. Mashable. Retrieved from https://mashable.com/2011/09/15/crowdfunding-history/#tdCpVANm28qT

Clifford, C. (Jan. 18, 2016). Less than a third of crowdfunding campaigns reach their goals. Entrepreneur Network. Retrieved from https://www.entrepreneur.com/article/269663

Cohn, S.R. (2012). The new crowdfunding registration exemption: Good idea, bad execution. Florida Law Review. Retrieved from https://scholarship.law.ufl.edu/cgi/viewcontent.cgi?article=1032&context=flr

Cornell, J.C. (2014). Crowdfunding: More than money jumpstarting university entrepreneurship. National Collegiate Inventors and Innovators Alliance.

Cowley, S. ()ct. 21, 2015). Indiegogo creates Generosity.com for personal fund-raising campaigns. Bits. Retrieved from https://bits.blogs.nytimes.com/2015/10/21/indiegogo-creates-generosity-com-for-personal-fund-raising-campaigns/

Creator Questions. (n.d.). Kickstarter. Retrieved from https://www.kickstarter.com/help/faq/creator+questions#faq_41823

Crowdfunding. (n.d.). In English Oxford Living Dictionaries. Retrieved from https://en.oxforddictionaries.com/definition/crowdfunding

Devaney, T. (2014, January 16). GOP: Crowdfunding rules a ‘deal-breaker’ for small businesses. The Hill. Retrieved from http://thehill.com/regulation/legislation/195715-gop-crowdfunding-rules-a-deal-breaker-for-small-businesses

Dushnitsky, G., Guerini, M., Piva, E., & and Rossi-Lamastra. C. (2016). Crowdfunding in Europe: Determinants of platform creation across countries. California Management Review. (58), 2. pp. 44-71. Retrieved from http://journals.sagepub.com/doi/pdf/10.1525/cmr.2016.58.2.44

Entrepreneurship (n.d.). In English Oxford Living Dictionaries. Retrieved from https://en.oxforddictionaries.com/definition/entrepreneurship

EVENTYS: Kickstarter Vs. Indiegogo – Which platform should you choose? (2018, April 4). Retrieved from https://enventyspartners.com/blog/kickstarter-vs-indiegogo-platform-choose/

Federal Securities Laws. (n.d.).

FitzGibbon, S.T. (1980, January). What is a Security? A redefinition based on eligibility to participate in the financial markets. Boston College Law School. Retrieved from https://lawdigitalcommons.bc.edu/cgi/viewcontent.cgi?referer=https://scholar.google.com/&httpsredir=1&article=1662&context=lsfp

Funding. (n.d.). Funding. Kickstarter. Retrieved from https://www.kickstarter.com/help/handbook/funding

Gabison, G.A. (2015). Equity crowdfunding: All regulated but not equal. DePaul Business & Commercial Law Journal. (13), 3, p. 359-409. Retrieved from https://web-a-ebscohost-com.proxy195.nclive.org/ehost/pdfviewer/pdfviewer?vid=1&sid=6f7d6740-e2ae-4d30-b821-dcc63f3c6710%40sessionmgr4007

Giudici, G., Nava, R., Lamastra, C.R., & Verecondo, C. (2012). Crowdfunding: The new frontier for financing entrepreneurship? Department of Management, Production and Industrial Engineering. Politecnico di Milano. Retrieved from https://ssrn.com/abstract=2157429

Groshoff, D., Urien, K., & Nguyen, A. (2014). Crowdfunding 6.0” Does the SEC’s Fintech law failure reveal the agency’s true mission to protect – solely accredited – investors? Retrieved from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2483371

Harrington, K. (2015, May 22). New JOBS Act regulation A+ will be a game changer. Forbes. Retrieved from https://www.forbes.com/sites/kevinharrington/2015/05/22/new-jobs-act-regulation-a-will-be-a-game-changer/#1e5793717f3f

Hemingway, J.M., (2014). How Congress killed investment crowdfunding: A tale of political pressure, hasty decisions, and inexpert judgments that begs for a happy ending. Kentucky Law Journal Vol 103, 2013-2014. Retrieved from https://uknowledge.uky.edu/cgi/viewcontent.cgi?article=1117&context=klj

Husain, S., & Root, A. (2015). Crowdfunding for entrepreneurship. AlliedCrowds.

IPO Study, Fees and Expenses, n.a. (2016, March 7). IPO Fees and Expenses, IPO Journal.

Ivanov, V. & Knyazeva, A. (2017). U.S. securities-based crowdfunding under Title III of bthe JOBS Act. Securities and Exchange Commission. Retrieved from https://www.sec.gov/dera/staff-papers/white-papers/28feb17_ivanov-knyazeva_crowdfunding-under-titleiii-jobs-act.html

Justia. (1946). Certiorari To The Court of Appeals. Retrieved from https://supreme.justia.com/cases/federal/us/328/293/case.html

Kaartemo, V. (2017).The elements of a successful crowdfunding campaign: A systematic literature review of crowdfunding performance. International Review of Entrepreneurship, (15) 3, pp. 291-318. Retrieved from https://web-a-ebscohost-com.proxy195.nclive.org/ehost/pdfviewer/pdfviewer?vid=2&sid=4cb9d514-7a85-4318-8723-8f7f79755165%40sessionmgr4010

Kauffman Foundation. (2016). The economic impact of high-growth startups. Kansas City, Missouri. Retrieved from https://www.kauffman.org/what-we-do/resources/entrepreneurship-policy-digest/the-economic-impact-of-high-growth-startups

Li, J., Chen, X., Kotha, S., & Fisher, G. (2017). Catching fire and spreading it: A glimpse into displayed entrepreneurial passion in crowdfunding campaigns. Journal of Applied Psychology. (102), 7, pp. 1075-1090.

Looking Back. (Dec. 21, 2017). Looking back on a year of clever things for curious humans.

Mazerov, M. (2016). Startups fuel job growth, animated. Center on Budget Policy Priorities. Retrieved from https://www.cbpp.org/blog/startups-fuel-job-growth-animated

Mollick, E. (2014). The dynamics of crowdfunding: An exploratory study. Journal of Business Venturing. (29), pp. 1-6.

Mollick, E. R. (2016). Containing multitudes: The many impacts of Kickstarter funding. University of Pennsylvania – Wharton School. Retrieved from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2808000.

Moreau, E. (Jan. 12, 2018). Lifewire.

Prive, T. (NOV 6, 20120. Inside the JOBS Act: Equity Crowdfunding. Forbes Magazine. Retrieved from https://www.forbes.com/sites/tanyaprive/2012/11/06/inside-the-jobs-act-equity-crowdfunding-2/#cfa29f54b2e7

Quaadman, T. (2017, March 22). Statement of the U.S. Chamber of Commerce.

Regulation D Offerings. (n.d). Retrieved from https://www.sec.gov/fast-answers/answers-regdhtm.html

Saska, J. (2014, June 23). Kickstarter but with a stock. Moneybox. Retrieved from http://www.slate.com/articles/business/moneybox/2014/06/sec_and_equity_crowdfunding_it_s_a_disaster_waiting_to_happen.html

Schein, D.D. & Trautman, L.J. (2019). The Dark Web and Employer Liability. Colorado Technology Law Journal (18, forthcoming). Retrieved from http://ssrn.com/abstract=3251479

Schweinbacher, A., & Larralde, B. (2010). Crowdfunding of small entrepreneurial ventures. Handbook of Entrepreneurial Finance. Oxford University Press. Oxford, England, UK

SEC Approves JOBS Act Requirement. (2013, July 10). Retrieved from https://www.sec.gov/news/press-release/2013-124-sec-approves-jobs-act-requirement-lift-general-solic

SEC Issues Proposal on Crowdfunding. (2013). Retrieved from https://www.sec.gov/news/press-release/2013-227

Securities and Trust Indentures, section 77b, (1). (n.d). Chapter 2A – Securities and trust Indentures. R

Selinber, G.B. (2015, January, 22). FAQs about securities for start-ups. Fairfield and Woods, P.C.

Shopify (n.d.). Indiegogo: Benefits and Drawbacks. Retrieved from https://www.shopify.com/guides/crowdfunding/indiegogo-benefits-drawbacks

Small Business Compliance Guides. (n.d.). Retrieved from https://www.sec.gov/info/smallbus/secg.shtml

Stansbury, M. (2014, June 24). The rules of Regulation D: Selling equity securities without a securities registration. Stansbury Weaver, Limited. Retrieved from http://www.stansburyweaver.com/the-rules-of-regulation-d-selling-equity-without-a-securities-registration/

The History of Crowdfunding (n.d.). Retrieved from https://www.fundable.com/crowdfunding101/history-of-crowdfunding

Terry, H.P., Schwartz, D., & Sun, T. (2015). The Future of Finance. Goldman Sachs.

Trautman, L.J. (2013). Who Qualifies as an Audit Committee Financial Expert Under SEC Regulations and NYSE Rules? DePaul Business and Commercial Law Journal (11) 205. Retrieved from http://www.ssrn.com/abstract=2137747

Trautman, L.J. & Michaely, G. (2014). The SEC & the Internet: Regulating the Web of Deceit. The Consumer Finance Law Quarterly Report (68) 262-281. Retrieved from http://www.ssrn.com/abstract=1951148

Trautman, L.J. (2016a). Is Disruptive Blockchain Technology the Future of Financial Services? The Consumer Finance Law Quarterly Report (69) 232. Retrieved from http://ssrn.com/abstract=2786186

Trautman, L.J. (2016b). E-Commerce and Electronic Payment System Risks: Lessons from PayPal. U.C. Davis Business Law Journal (17) 261. Retrieved from http://ssrn.com/abstract=2314119

Trautman, L.J. (2016c). Who Sits On Texas Corporate Boards? Texas Corporate Directors: Who They Are and What They Do. Houston Business and Tax Law Journal (16) 44. Retrieved from http://ssrn.com/abstract=2493569

Trautman, L.J. (2016d). Managing Cyberthreat. Santa Clara Computer & High Technology Law Journal (33) 230. Retrieved from http://ssrn.com/abstract=2534119.

Trautman, L.J., Anthony “Tony” Luppino & Malika S. Simmons (2016). Some Key Things U.S. Entrepreneurs Need to Know About The Law and Lawyers. Texas Journal of Business Law (46) 155 (2016), Retrieved from http://ssrn.com/abstract=2606808

Trautman, L.J. (2017). The Board’s Responsibility for Crisis Governance. Hastings Business Law Journal (13) 275. Retrieved from http://ssrn.com/abstract=2623219

Trautman, L.J. & Harrell, A.C. (2017). Bitcoin Versus Regulated Payment Systems: What Gives? Cardozo Law Review (38) 1041. Retrieved from http://ssrn.com/abstract=2730983

Trautman, L.J. (2018a). Bitcoin, Virtual Currencies and the Struggle of Law and Regulation to Keep Pace. Marquette Law Review (102) 447-538. Retrieved from https://ssrn.com/abstract=3182867

Trautman, L.J. (2018b). How Google Perceives Customer Privacy, Cyber, E-Commerce, Political and Regulatory Compliance Risks. William and Mary Business Law Review (10) 1- Retrieved from https://ssrn.com/abstract=3067298

Trautman, L.J. & Janet Ford (2018). Nonprofit Governance: The Basics. Akron Law Review (52) 971-1042. Retrieved from https://ssrn.com/abstract=3133818

Trautman, L.J. & Ormerod, P.C. (2018). Industrial Cyber Vulnerabilities: Lessons From StuxNet and the Internet of Things. University of Miami Law Review (72) 761. Retrieved from http://ssrn.com/abstract=2982629

Trautman, L.J. & Molesky, M.J. (2019). A Primer for Blockchain. UMKC Law Review (88:1). Retrieved from http://ssrn.com/abstract=3324660

Trautman, L.J. & Ormerod, P.C. (2019). WannaCry, Ransomware, and the Emerging Threat to Corporations. Tennessee Law Review (86) 503-556. Retrieved from http://ssrn.com/abstract=3238293

United Housing Foundation Inc. v. Forman. (n.d.). Retrieved from https://www.quimbee.com/cases/united-housing-foundation-inc-v-forman

Updated: Crowdfunding and the JOBS Act: What Investors Should Know. (n.d.). Retrieved from http://www.finra.org/investors/alerts/crowdfunding-and-jobs-act-what-investors-should-know

U.S. Code & 77d – Exempted transactions. (n.d.). Retrieved from https://www.law.cornell.edu/uscode/text/15/77d

Vealey, K.P., & Gerding, J.M. (2016). Rhetorical work in crowd-based entrepreneurship: Lessons learned from teaching crowdfunding as an emerging site of professional and technical communication. IEEE Transactions on Professional Communication. (59) 4, pp. 407- 427.

Venture Choice. (n.d.) Private Placements of Securities: Rule 504, 505, and 506. Retrieved from http://www.venturechoice.com/articles/rule_504_505_506.htm

Wiens, J., & Bell-Masterson, J. (June 2, 2015). How entrepreneurs access capital and get funded. The Kauffman Foundation. Retrieved from http://www.kauffman.org/what-we-do/resources/entrepreneurship-policy-digest/how-entrepreneurs-access-capital-and-get-funded

Zouhali-Worrall, M. (n.d.). Comparison of crowdfunding websites. Inc. Retrieved from https://www.inc.com/magazine/201111/comparison-of-crowdfunding-websites.html

View Profile

View Profile