How Tech Startups Protect Against the Downside of Corporate Venture Capital

Many large corporations are making corporate venture capital (CVC) investments in tech startups. While the innovation benefits for these corporations have received much attention in the business press and academia, less is known about the startup’s perspective. When dealing with giants (corporations), how does the dwarf (startup) avoid getting crushed? This article, based on our research, shows startups how to weigh the benefits and risks of working with a CVC and some of the safeguards they can put in place to protect their interests in this uneven yet potentially fruitful partnership.

The Rise of Corporate VC

Many venture capital firms are independent firms, but some are set up by corporations. When they are, this is called “corporate venture capital.” Independent VCs have 10 times the share of startup investment deals as VCs set up within companies, but corporate venture capital (CVC) has rapidly gained momentum in the past few years. Large CVC investors like Intel Capital and Google Ventures (GV) have attracted much media attention, and globally there were over 4,500 CVC-backed deals in 2021, more than twice the number in 2016. More than 200 new CVCs were launched last year alone.

Large corporations like Alphabet (parent of Google) even have multiple CVC vehicles, some of which are focused on particular technologies. For example, Gradient Ventures centers on AI startups. We’ve also seen that midsize firms with more limited financial means can engage in CVC by joining forces and setting up pooled CVC funds.

What’s behind this surge? One key factor is the ongoing digital transformation of industries, in which new technologies are being introduced to automate and augment business operations. For example, some of the hottest CVC areas include AI, fintech, and digital health. Startups are disrupting entire sectors with new digital technologies and innovative business models, and established corporations feel the need to track these developments and adjust their capabilities and systems accordingly. In this way, CVC has become an integral part of many companies’ innovation strategy to help them be more agile in a constantly changing technology environment.

The benefits of CVC for established corporations are well-documented: getting a ringside seat to new technology development can open up new sources of revenue and new opportunities for innovation. As stated by former Intel Capital president Wendell Brooks at the 2017 CES event, “we are the eyes and ears of what the world will look like 10 years from now.” In academia, CVC is often framed as a wait-and-see approach: by holding a portfolio of minority stakes in startups, corporate managers can monitor several tech developments at once and seize on the most promising ones through technology licensing or acquisition deals. CVC is a valuable complement to internal R&D and enables corporations to explore many new technologies at the same time, faster and with less risk.

However, the impact of CVC on the startup entrepreneurs hasn’t been as well researched. An important question comes to mind: when dealing with giants, how does the dwarf avoid getting crushed? Existing research has revealed one obvious risk for the smaller firm: having intellectual property exploited by the larger firm (referred to as “IP misappropriation.”) But our own research told us that entrepreneurs actually don’t see this as the biggest risk, since they know that big companies are wary of the reputational damage that could happen if news of misappropriation gets around. We spoke with 14 early-stage tech founders, co-founders and investors in the US and Europe to get their thoughts on the benefits and threats of CVC for startups, and discovered some useful tactics employed by startups to protect against the downside risk of CVC.

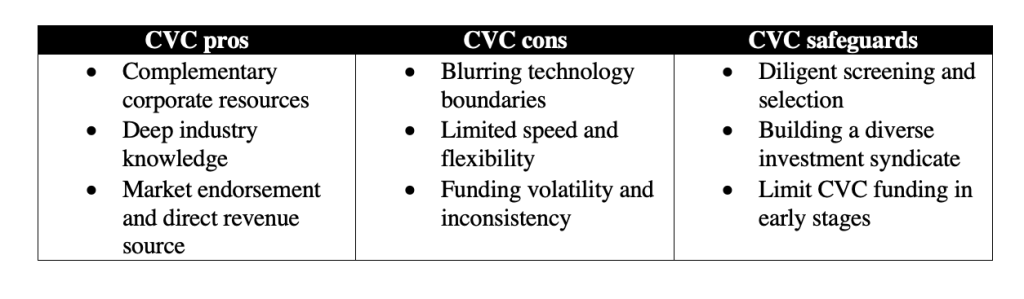

A summary of what they told us can be found in the table below.

Benefits of CVC for startups

Clearly startups benefit greatly from the capital their CVC partner can provide, but our respondents told us this is not the only advantage or even the most important one. The money can also be raised from other investors, including independent VCs who often have longer track records and deeper expertise in startup financing. While independents once called CVC “dumb money,” CVCs have actually grown larger and more experienced and can offer several advantages beyond investment. The founders and investors who spoke to us outlined these three.

Complementary Resources

Corporations can give entrepreneurs access to useful technologies, specialized equipment, production capacity, marketing support, or global distribution channels that help them move their innovation to market faster. The co-founder of a Spanish biotech startup told us, “CVCs give you access to something beyond capital. You can reduce your CapEx (capital expenditures) and piggyback on their investments made, and they provide their portfolio companies with distribution channels.”

A Guide Through Uncharted Territory

Some sectors can be very challenging to navigate for inexperienced startups. Consider the healthcare sector, which has many different stakeholders – governmental agencies, insurance companies, public and private healthcare providers – along with a thick and complex regulatory framework that differs from one country to the other. Here, a fledging healthtech startup will find great value in the support and industry-specific know-how of corporate investors like Philips or Roche who, as legacy firms, have been embedded in the healthcare ecosystem for many years and can reduce the small venture’s risks and uncertainties.

Legitimacy and Sales

Startup ventures have no track record and may lack credibility in the market. Prospective clients may not want to take the risk of buying something from a new and unknown company. Being backed by a well-known large corporation boosts the venture’s legitimacy, which helps convince clients to place orders. This “endorsement effect” of CVC is stronger for the general public than that of lesser-known independent VCs. B2B startups are also attracted to the possibility that their CVC investor will become a major client. The co-founder of a German SaaS startup told us: “Ideally the corporate investor becomes a large customer and presents a source of potential revenue for us.”

Concerns when seeking CVC funding

Based on our interviews, we identified three main concerns for startups that arise when accepting CVC funding:

Technology ‘Grey Areas’

As we mentioned, the founders and investors we spoke with were less concerned about having their intellectual property stolen away by the corporate investor, because the larger firm would face great reputational damage if the word got around of their piracy. But they identified a more subtle and indirect risk, captured in this statement: “We started getting a lot of interest to start doing joint projects, mixing technologies and getting into sort of grey areas. This can potentially limit your technology as a standalone, because at a later stage they may only want to use this mixed product instead of your solo product.”

Joint projects and incorporating corporate tech can certainly be beneficial in some situations, but a naïve approach to IP and mixing of technologies may limit the standalone market potential of the startup’s tech and make them too dependent on the larger firm. That is, in joint projects with a powerful corporate investor it can be challenging to keep the startup’s technology sufficiently separate or freestanding. This is something entrepreneurs should bear in mind.

Bureaucracy and Limited Flexibility

CVC funds are usually structured as divisions within companies and may lack the mindset of independent VCs with regard to managing startup portfolios. Many CVC staff members have never worked anywhere else but in the corporate world, which is known for being “slow and bureaucratic,” said a German co-founder of an EdTech startup. It takes too long to make a decision, and often the startup gets drawn into the company’s policies and regulations and lose flexibility as a result. CVC funding can even limit startups’ ability to operate freely in the open market. Other players may be reluctant to work with startups partially owned by their rivals; and exclusivity clauses set forth in the investor’s agreement may hinder such B2B operations, lowering the market potential of the startup. “Some corporates are very restrictive and don’t want competitors becoming customers or engaging in any form with the startup,” the GP of a European CVC fund told us.

Ever-Shifting Priorities

Due to their strategic nature, CVC programs are often cyclical. They invest more heavily during periods of major technological shifts like the ongoing digital transformation or e-mobility revolution, but can quickly change course and pull the plug when strategic priorities shift, leading to underinvestment along the startup’s life cycle. A similar observation was already made by Henry Chesbrough back in 2002, stating that “while private VC investments also ebb and flow as the economy changes, the shifts in corporate VC investments have been particularly dramatic.”

Large companies react strongly and quickly to macro events that affect their top line of business, and their CVC arm may be one of the first to be downsized to boost cash flow. The big company’s strategy may also shift during the lifecycle of a startup, as strategic plans are updated every three to five years. The result is volatility and inconsistency in CVC programs and their investments. Furthermore, once the corporate has learned sufficiently about the startup’s technology, it can shift attention away from the partnership. As stressed by a Portuguese founder active in the automotive sector: “If conditions of the market change or the strategy of the parent company changes, the CVC unit can underinvest in the relationship and stop supporting the growth of the startup.”

These three concerns and others are reflected in a quote by the co-founder of a US EdTech startup, who said this about CVC: “It sends a negative signal for follow-on rounds, because all the other investors and independent VC funds will be more reluctant, as they are afraid that the corporate may want to take strategic control and has different interests than institutional investors.”

Safeguards Against CVC risks

Startups must put safeguards in place that let them exploit the benefits of CVC funding and cope with the concerns proactively. In addition to conventional contractual stipulations -- regarding items like IP, share transfers, preemptive or drag-along rights or protective provisions -- the founders we spoke with gave us other useful pieces of advice.

Be Pickier

First, realize that picking a partner is a two-way street, and small ventures don’t have to say yes. Our interview subjects told us that many tech startups can be just as discerning as investors picking ventures to finance. Startups should look at these factors to understand what the CVC can bring to the table and how the relationship will likely play out:

- The CVC’s established track record in terms of helpful and trustworthy behavior;

- The autonomy of the CVC unit from its corporate parent, which may translate to higher operational speed;

- The background of CVC staff members, with a preference for former entrepreneurs and independent VC investment managers;

- The potential for adding to (complementing) rather than replacing or competing with (substituting) the corporate parent’s offerings; this holds equally true for any of the corporate’s subsidiaries and other portfolio startup ventures.

A French CVC investor pointed out that “the most valuable and high-potential startups may avoid CVC investments if these points raise red flags.” Another founder emphasized that “it’s crucial to look at the historic track record, not in terms of capital gains but in terms of how the fund behaved in previous investments.” Consider whether the CVC has a track record and reputation for ensuring mutual advantage from the equity alliance, commitment to the relationship and continuity of their investment programs (e.g., by providing follow-up funding). This signals that they are encouraging startups to approach them with new technologies. In short, promising tech startups can screen and select, just like investors.

Consider More than One Investor

The size of the equity stake sold to the CVC has direct implications for its power and influence. A co-founder of a German SaaS startup stressed that “to grow as an independent entity, we can’t have a corporate investor controlling us too much; therefore we are pulling in other private investors and VCs into the round, at the same terms.” To reduce the risks of CVC, startups should structure the investment deal as a diverse investment syndicate, which preserves their decision-making autonomy and operating flexibility. In an investment syndicate, multiple investors co-invest in a startup's funding round.

Our interview partners told us that a syndicate where an independent VC is the lead investor and the CVC’s ownership remains on the lower end of a minority passive stake – meaning well below 20% – offered them the most protection. A diverse investment syndicate also lets the startup tap their investment partners’ different skill sets. While CVCs are comparably more effective in “commerce building” by giving startups access to the parent’s resources and sales channels, independent VCs are more effective in “enterprise nurturing” by assisting with arranging financing rounds and recruiting key personnel.

Optimize Your Timing

Tech startups face a critical decision: when to enter a CVC investment relationship? In 2021, more than half of CVC-backed deals were early-stage.Collaborating early can secure access to vital external resources and reduce time-to-market. Although CVC deals are dominated by early-stage involvement, several of the startups we interviewed argue that later-stage ventures can more easily exploit the benefits of CVC and overcome its hurdles. They say most CVCs don’t have the flexibility and tools to provide the hands-on support that startups need at an early development stage.

Furthermore, startups with mature and better-established technologies are less exposed to the type of indirect threat to their IP we talked about earlier: when the bigger firm uses bits and pieces of the startup’s technology that become hard for the startup to reclaim when the partnership ends. Later-stage startups have also gained fundraising experience and developed a set of routines that allow them to better screen and select suitable CVCs. Clearly this timing decision involves a tradeoff, but our interviews point out that startups that are farther along are better equipped to safeguard their technology as a standalone.

Conclusion

Global CVC-backed funding is on the rise, reaching an all-time high in 2021, and it holds great potential for synergies between resource-rich yet slow corporates and agile innovative startups. Corporates can gain deep insight in emerging technologies and business models to infuse their innovation strategy, and startup ventures can profit from their complementary resources, industry expertise, and endorsement. Tech startups can benefit tremendously from the abundance of CVC capital in the market, as long as they are aware of the pitfalls and mitigate them proactively.

ABOUT THE AUTHORS

Yannick Bammens is Associate Professor of Strategy & Entrepreneurship at Maastricht University in the Netherlands. His research has been published in various journals including Journal of Management, Journal of Management Studies, and Harvard Business Review. Starting January 2023, he will join Hasselt University in Belgium

Jakob Lilienweiss is Investment Analyst specialized in healthcare at High-Tech Gründerfonds (HTGF), one of Germany’s most active venture capital firms.

REFERENCES

Y. Bammens & P. Hünermund (2021). “How midsize companies can compete in AI”. Harvard Business Review: https://hbr.org/2021/09/how-midsize-companies-can-compete-in-ai

CB Insights (2020). “The 2020 global CVC report”: https://www.cbinsights.com/reports/CB-Insights_CVC-Report-2020.pdf

CB Insights (2021). “State of CVC”: https://www.cbinsights.com/reports/CB-Insights_CVC-Report-2021.pdf

M. Ceccagnoli, M. Higgins & H. Kang (2018). “Corporate venture capital as a real option in the markets for technology”. Strategic Management Journal, vol. 39, pp. 3355-3381: https://onlinelibrary.wiley.com/doi/abs/10.1002/smj.2950

H. Chesbrough (2002). “Making Sense of Corporate Venture Capital”. Harvard Business Review: https://hbr.org/2002/03/making-sense-of-corporate-venture-capital

J. Eckblad, T. Gutmann & C. Lindener (2019). “Report on global corporate venturing research data”: https://www.corporateventuringresearch.org

View Profile

View Profile